2. Learn Your Options

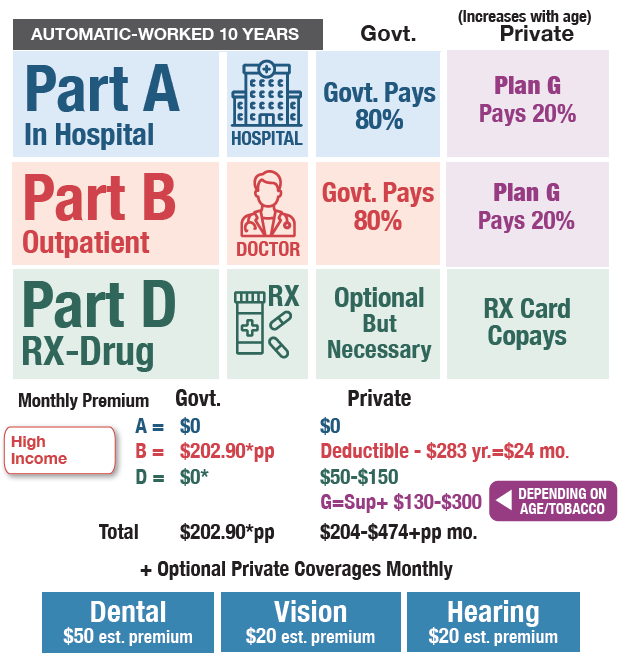

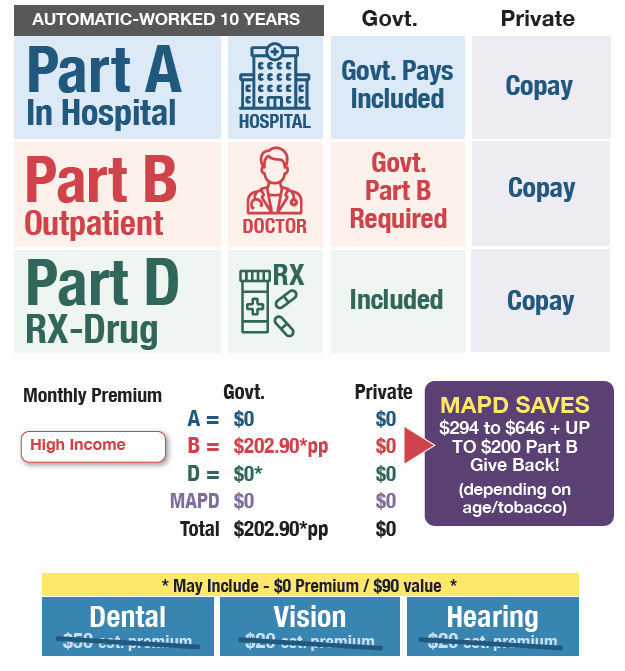

After enrolling in Medicare, which pays 80% of your medical bills, you will need to decide how to cover the remaining 20%. This is one of the most important decisions you’ll make, because it affects not only your current costs, but also your long-term financial stability.

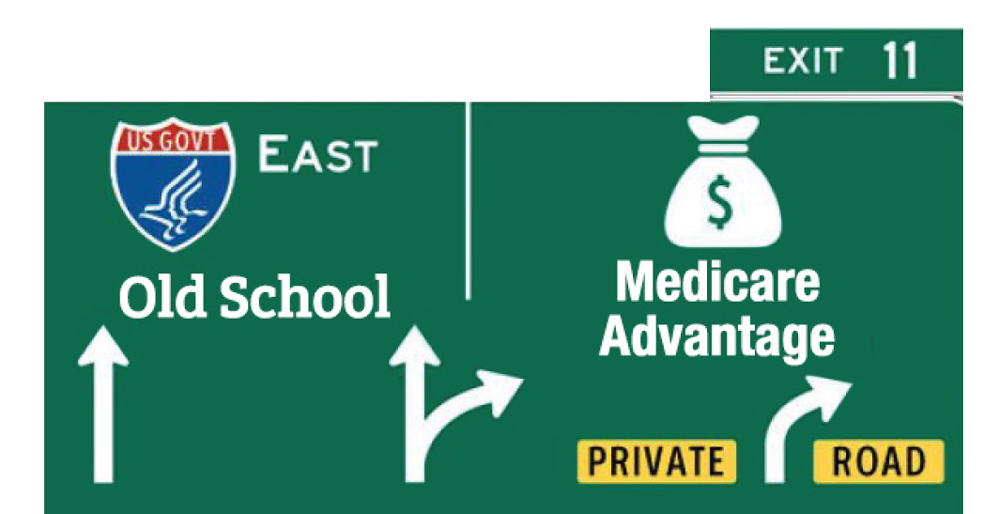

You have two primary paths to choose from.

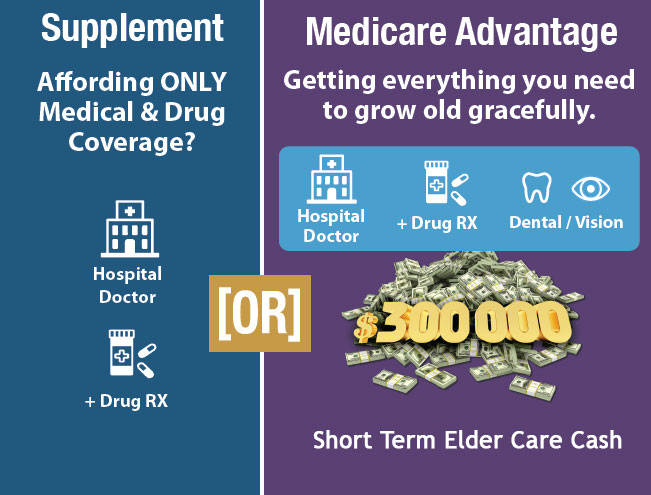

One option is to stay with Original Medicare and add a Medicare Supplement plan, which helps cover the remaining 20% of medical expenses.

The other option is to choose a Medicare Advantage plan, which replaces Original Medicare with a bundled, all-in-one alternative offered through private insurance.

Both options work well but the premiums are dramatically different not only now but much more so in the future.

This decision isn’t just about today, it’s about your entire life journey. Choosing the wrong path could mean overpaying in one area while leaving yourself exposed in another. The goal is to understand how each option works so you can move forward with clarity and confidence.